The Dividend Standard

Institutional-grade research for investors building a rising income stream. One company at a time.

A high yield tells you what a company pays today. It tells you nothing about whether that payment will still be growing when you need it.

The Dividend Standard is built around the harder question: will this dividend keep compounding for the next ten or twenty years?

Most dividend research answers by looking backward, at the streak of past increases. That tells you what a company has done. It says very little about what it can do next. The dividends that matter to a retirement are the ones still ahead of you, and those are funded by the returns a business earns on the capital it reinvests.

So every issue starts there.

One high-quality company, broken down by the moat that protects the cash, the returns on capital that compound it, the balance sheet that guarantees it, and the reinvestment runway that tells you how much dividend growth is still in the tank. One business per issue.

Why dividend growth, and not dividend yield

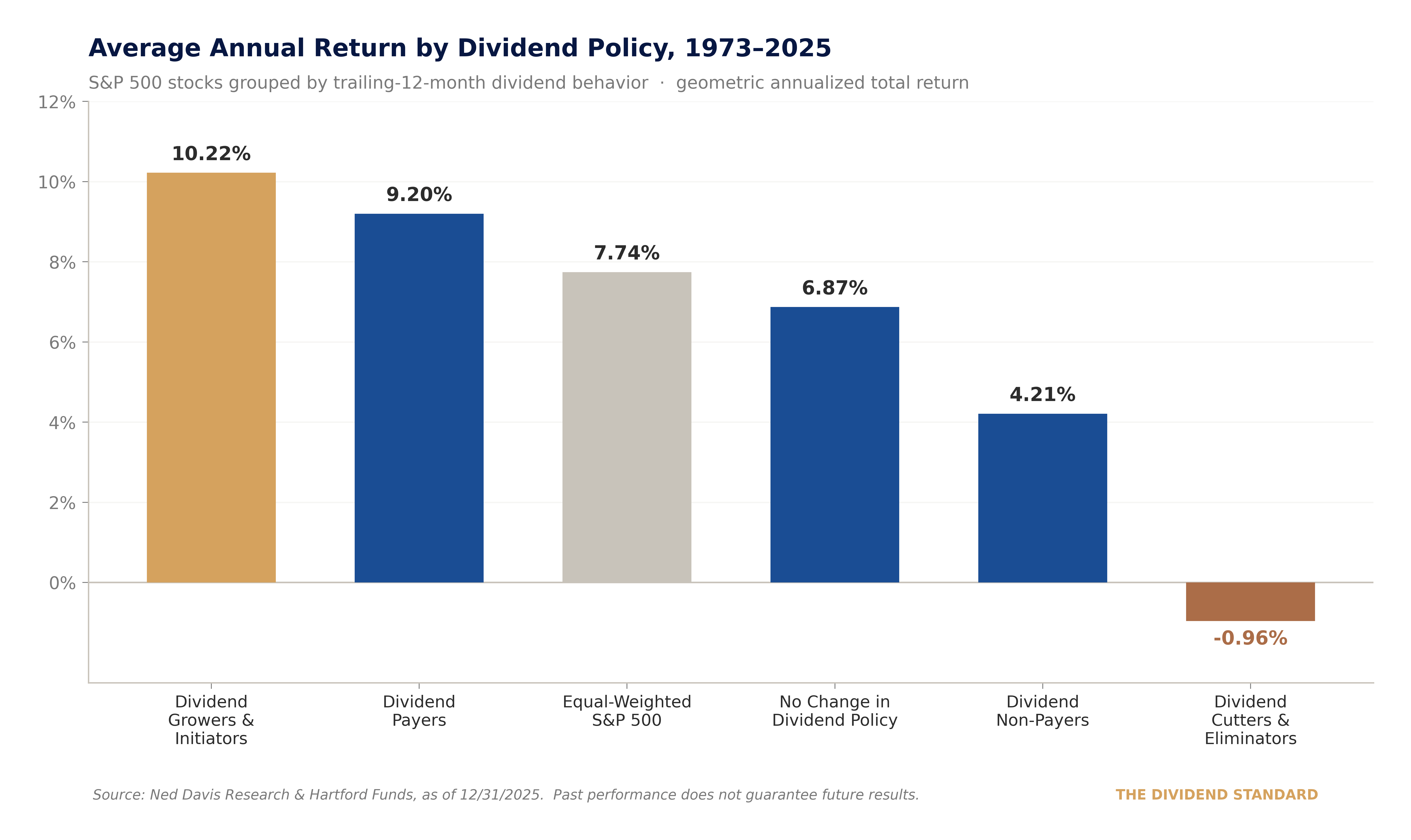

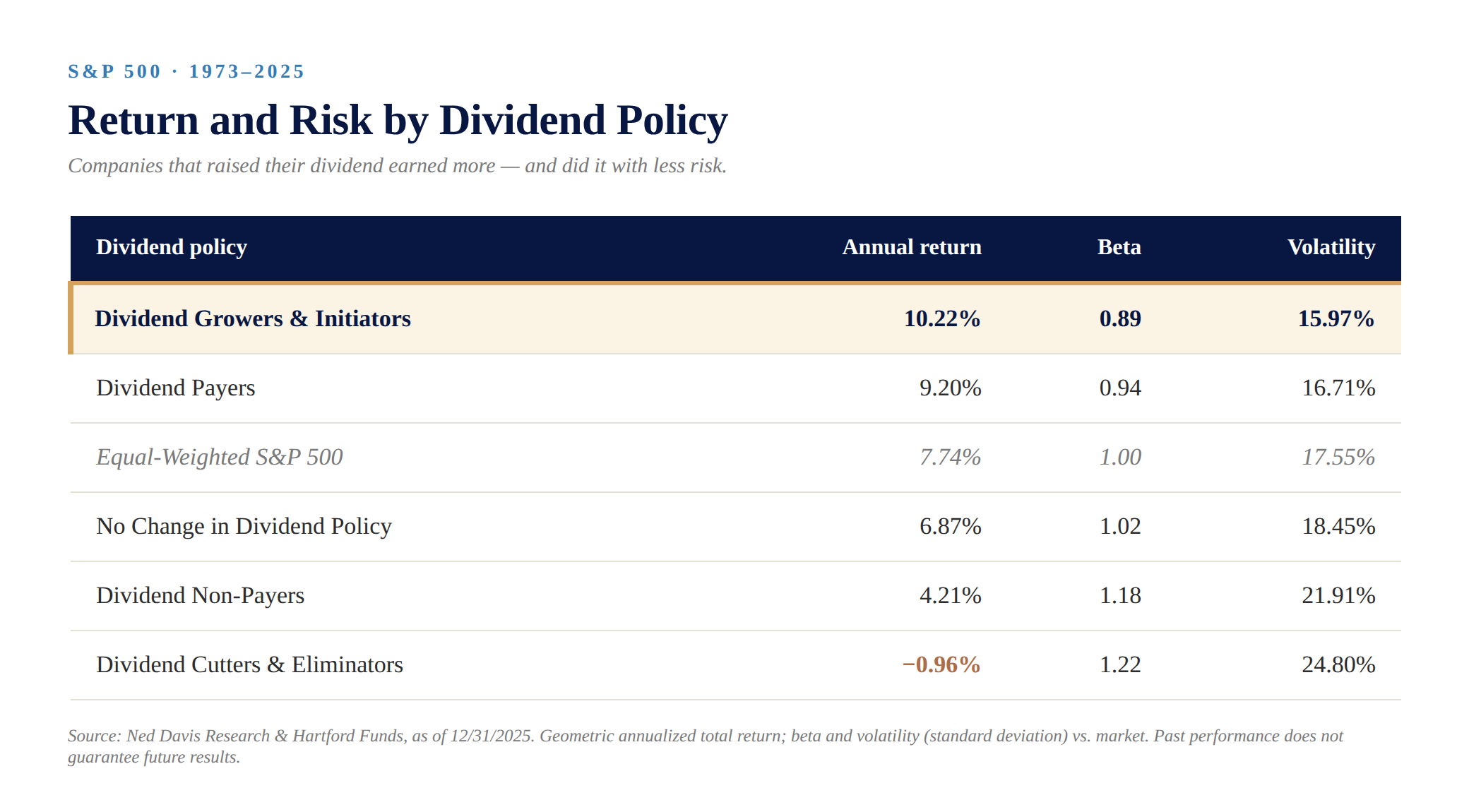

Ned Davis Research and Hartford Funds have tracked S&P 500 companies grouped by what they do with their dividend, going back to 1973.

Through the end of 2025, the companies that grew or initiated a dividend returned 10.22% a year. The ones that paid but didn’t grow, less. The ones that paid nothing, 4.21%. And the companies that cut or eliminated their dividend produced negative annual returns over more than five decades.

The growers didn’t just win on return. They won with less risk.

Higher return, lower beta, less volatility. That combination is rare, and it points at something real: a company that can raise its dividend year after year is telling you it generates more cash than it needs, earns a high return on what it keeps, and is run by people willing to commit to shareholders.

Since 1960, roughly 85% of the S&P 500’s cumulative total return has come from reinvested dividends and the compounding they produce, according to Hartford Funds. And it’s why every income investor should fear the bottom row. A dividend cut is not a small setback, it is a wealth event. Which is why dividend safety — whether free cash flow actually covers the payment — is never optional here.

What makes The Dividend Standard different

Three things set the research apart:

Returns on capital are the spine of every issue. I calculate ROIC and ROIIC — return on invested capital, and return on incremental invested capital — using the cash-tax methodology of Michael Mauboussin and Dan Callahan.

ROIC tells you how good the existing business is.

ROIIC tells you whether the next dollar the company reinvests is creating value or destroying it. That second number, combined with how much the business reinvests, is the closest thing there is to a forecast of future dividend growth.

The reinvestment runway, not the track record, drives the verdict. A twenty-year streak of increases is history. What I want to know is how long the company can keep raising the dividend. How large the market it serves still is, whether it has pricing power, and whether its high returns on capital can be sustained on a growing base. That runway is the barometer of the dividends still ahead of you.

A transparent score and a public record. Every company is scored 0–100 across five weighted dimensions — moat, free-cash-flow safety, dividend track record, ROIC/ROIIC quality, and management.

Who this is for

This is for the investor building a rising stream of income for the long term. A retirement that isn’t for decades, or one already underway.

You might be sophisticated or just starting out; what matters is that you want to understand the machine behind a dividend, not just its size. If you want to know why a payout is durable and what would break it.

It is not for the yield chaser.

If the goal is the highest number on the screen this week, there are other newsletters for that. The Dividend Standard trades the thrill of a big headline yield for the durability of an income stream that grows.

What you get

One deep-dive issue per month on a single high-quality dividend growth company — the full nine-part analysis, the score, the valuation, and a clear buy/watch/avoid verdict with a price. Between issues, I’ll send an update on a covered name only when the underlying business changes in a way that matters, for better or worse.

If you want research that treats a dividend as the output of a business rather than a number on a screen, subscribe below.

The Dividend Standard is independent research and commentary. It is not investment advice, and I am not your financial adviser. Do your own due diligence before buying or selling any security.