MSFT: The $3 Trillion Cornerstone Dividend

Microsoft’s dividend is safe but the real question is whether AI reinvestment can earn its keep.

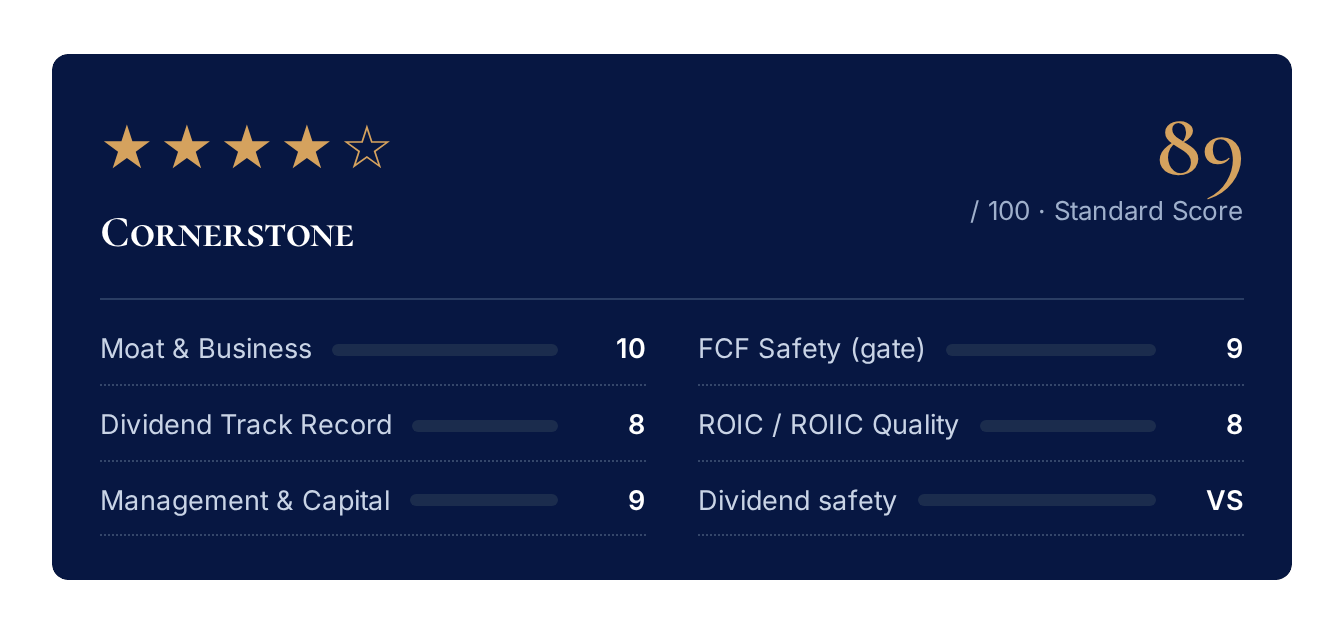

Microsoft’s yield is barely 1% but The Dividend Standard is not a yield-chasing letter. It is a letter about the machine behind the dividend: the moat that protects the cash, the returns on capital that compound it, and the balance sheet that guarantees it. On every one of those, Microsoft is close to the top of the table.

And yet it is not a five-star name.

It is held back by two specific things.

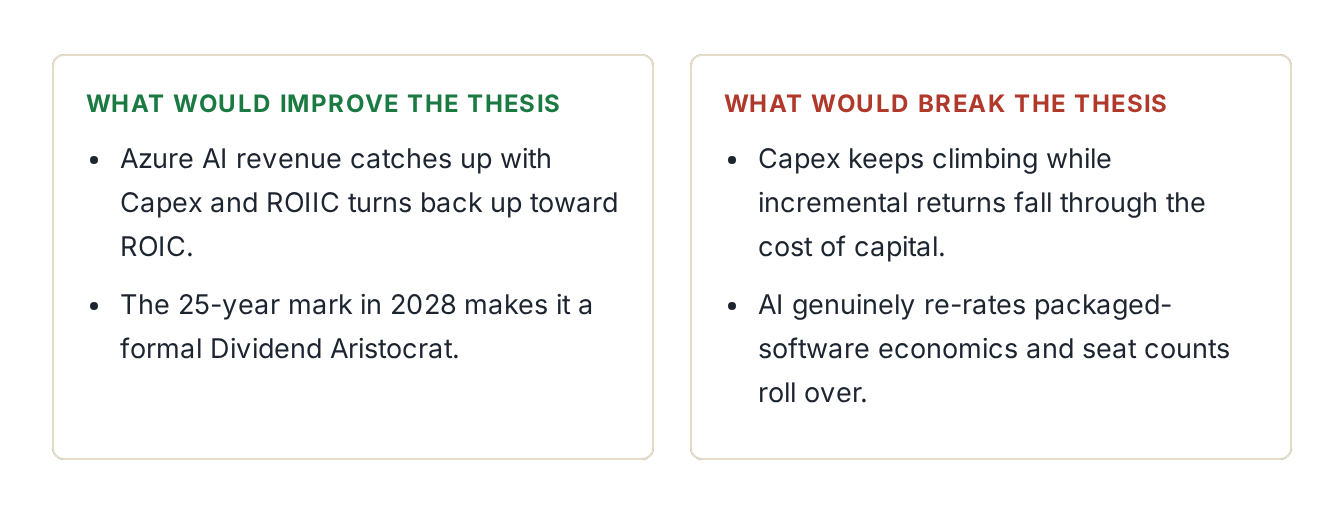

One is a calendar problem that fixes itself in 2028.

The other is the most important chart in this issue and the reason a dividend investor should care about a company spending $65 billion a year on data centers.

Business & Moat

Microsoft sells software and cloud computing to roughly every business on earth. It operates three divisions, each about a third of revenue.

Productivity: Office 365, Teams, Dynamics, LinkedIn. The tools companies run on.

Intelligent Cloud: Azure, the second-largest public cloud, plus the server software underneath it.

More Personal Computing: Windows, Xbox, search. Revenue was $282 billion in fiscal 2025 and grows mid-teens.

The load-bearing moat is switching costs. Once a company runs its email, its files, its identity system, and its financial reporting inside Microsoft’s stack, leaving means re-training every employee and re-wiring every workflow. Businesses don’t do that, it’s simpler to renew and keep renewing.

Barriers to entry. Competing with Azure means matching a hyperscale footprint in 60+ regions, with hundreds of data centers, and a capex bill running ~$65 billion a year (23% of revenue). Right now only two other companies on earth, Amazon and Alphabet, can write that check.

Network effects. Every Excel plug-in, Teams integration, and GitHub repo makes the suite stickier and raises the cost of leaving for the whole organization, not just one seat.

Scale advantages. Azure is the #2 public cloud at roughly a quarter of global infrastructure spend, behind AWS at about 30% and closing the gap while growing ~40% a year. That scale produces ~68% gross and ~45% operating margins, economics smaller rivals or those just starting out can’t match.

Pricing power is the tell that all of this is real: Microsoft raises seat prices and moves customers to richer SKUs year after year without losing them.

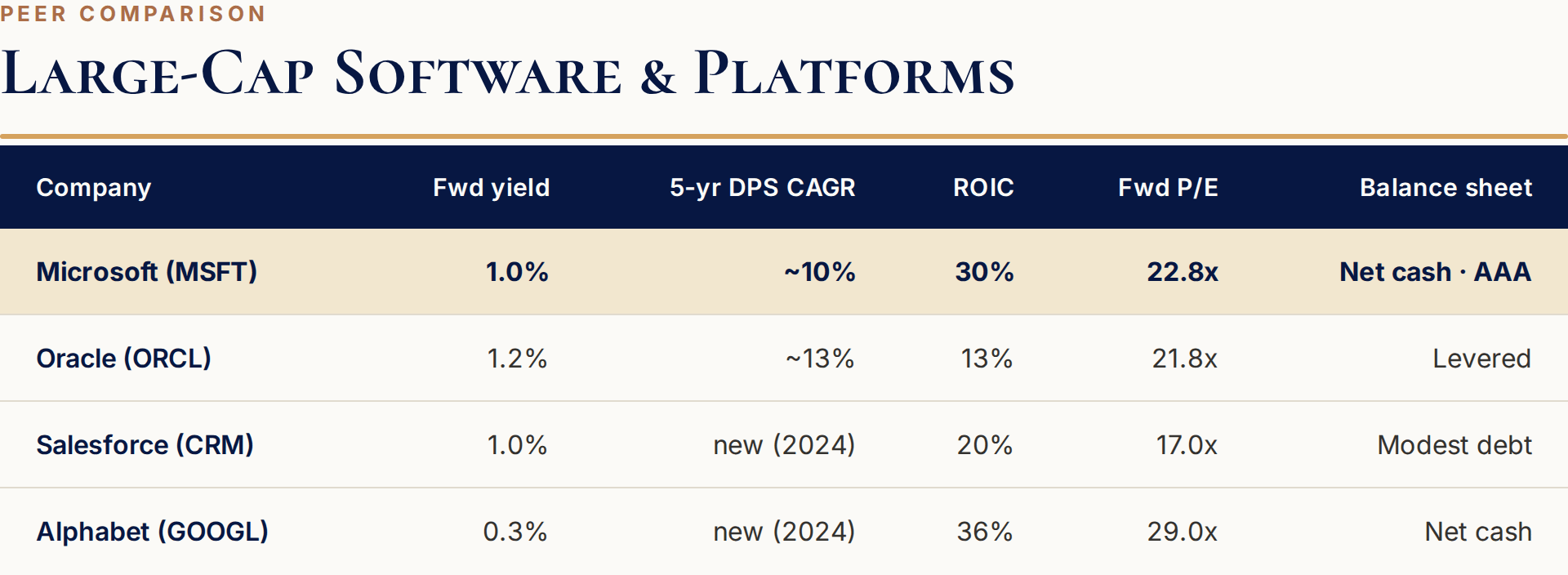

The moat in three numbers: a rising ~20–25% share of the cloud-infrastructure market; ~45% operating margins against low-teens-to-30% for peers; and a 30% ROIC that runs 2–3x its closest software comps (Oracle 13%, Salesforce 20%).

The one risk to the moat. The same AI wave that helps Azure could, over a decade, let companies “vibe-code” their way around packaged application software. It’s not one new competitor but thousands of small ones. I think this hits Microsoft’s application peers harder than Microsoft itself but it is a risk to watch over the next decade.

Dividend History & Growth

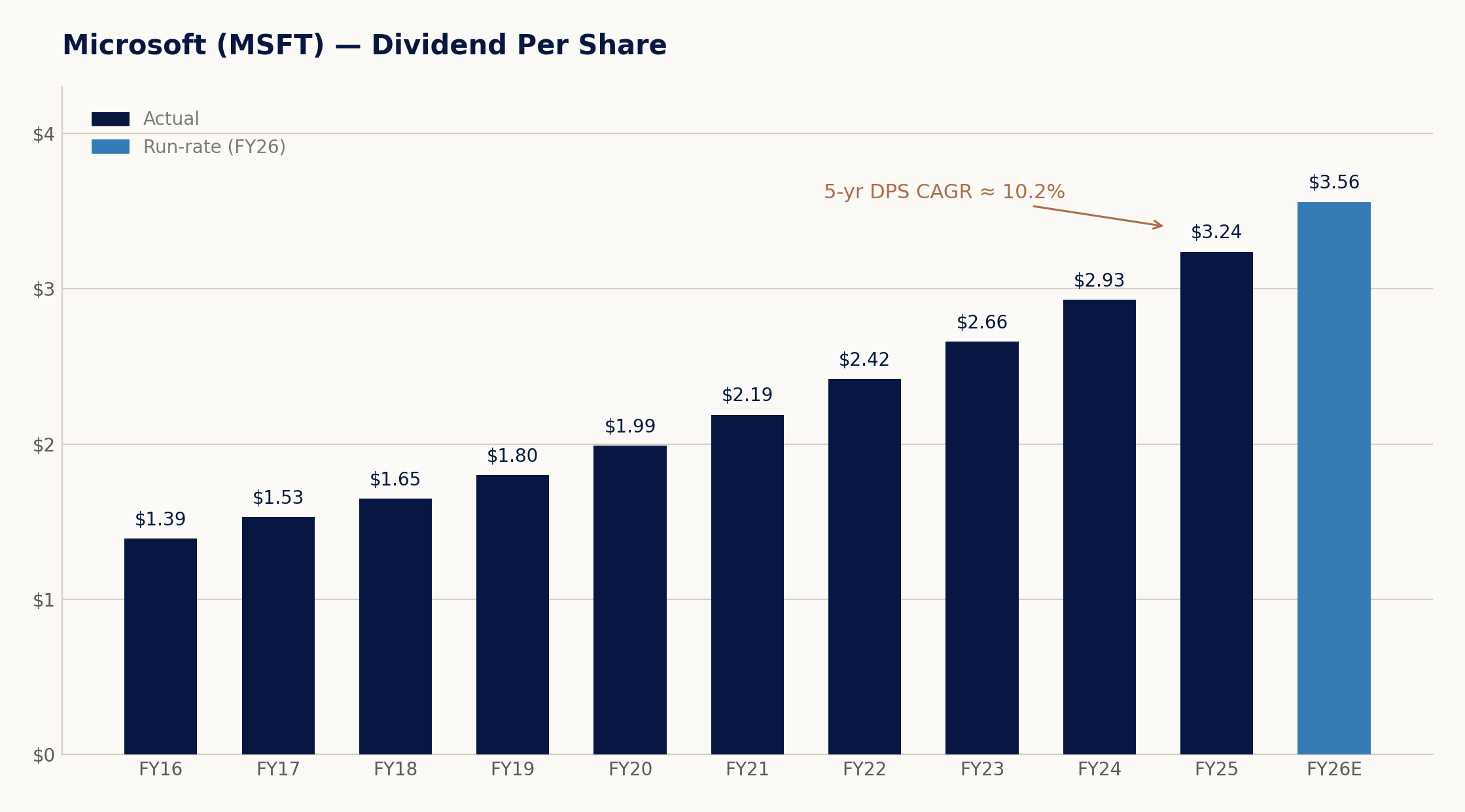

Microsoft has raised its dividend every year since 2003, 23 straight years of increases. That is the longest unbroken raise streak in the “Magnificent Seven.” It is not yet a Dividend Aristocrat (that takes 25 years), but it crosses the line in roughly 2028.

The raises are consistent at roughly 10% a year and similar across the 1-, 3-, 5- and 10-year windows. The most recent quarterly bump was $0.83 to $0.91, a 9.6% increase. Fiscal 2026 will pay $3.56 per share.

FCF Coverage & Balance Sheet

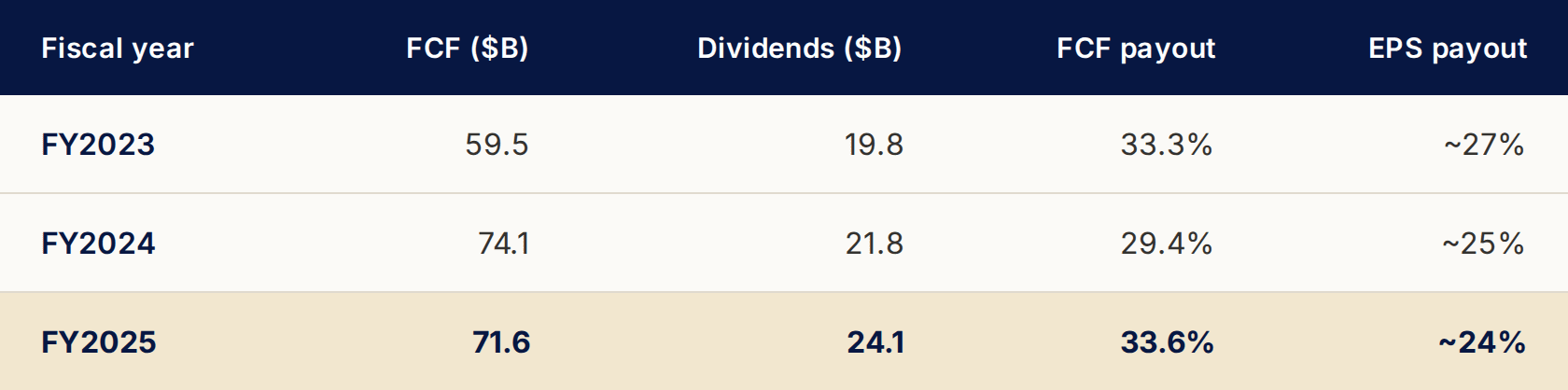

Earnings-based payout ratios are the starting point. I want to see the dividend covered by free cash flow. Can the company adequately cover its dividend with the cash left after it funds itself?

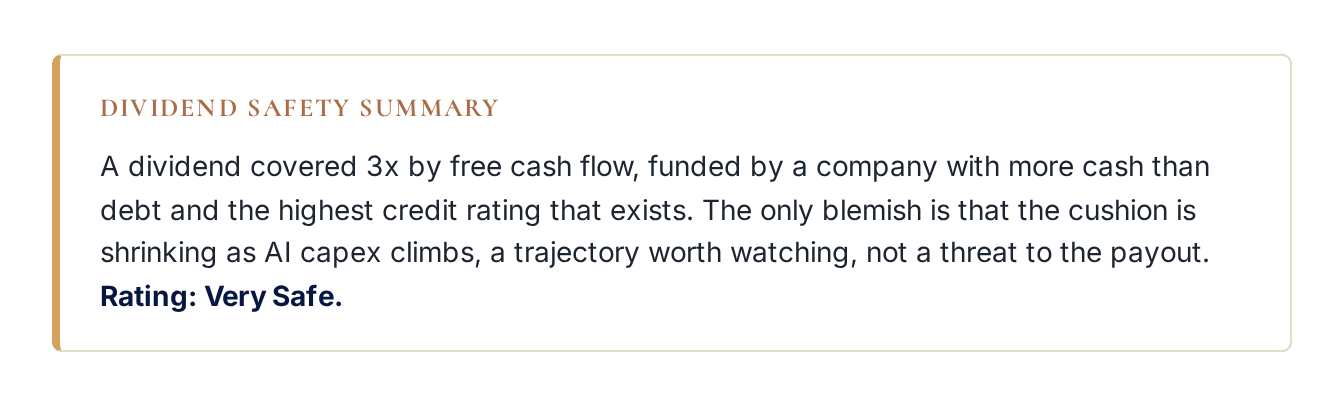

In fiscal 2025 Microsoft generated $71.6 billion of FCF and paid out $24.1 billion in dividends. That’s a 33.6% FCF payout. The dividend is covered three times over

FCF stopped growing in fiscal 2025 even as net income kept climbing, because capital spending exploded. Capex hit 23% of revenue and is heading toward 30%+ as Microsoft pours concrete and GPUs into AI data centers.

The dividend is still well covered, but the cushion is being spent. On the current trajectory the forward FCF payout drifts toward the mid-40s. Still safe but not improving.

Their balance sheet strength helps alleviate the capex spending concerns

Microsoft holds $94.6 billion in cash and investments against $60.6 billion of debt, a net cash position.

Net debt to EBITDA is negative.

Interest coverage is north of 50x. And their credit rating is AAA / Aaa, from both S&P and Moody’s. Microsoft is one of only two U.S. public companies that can say that.

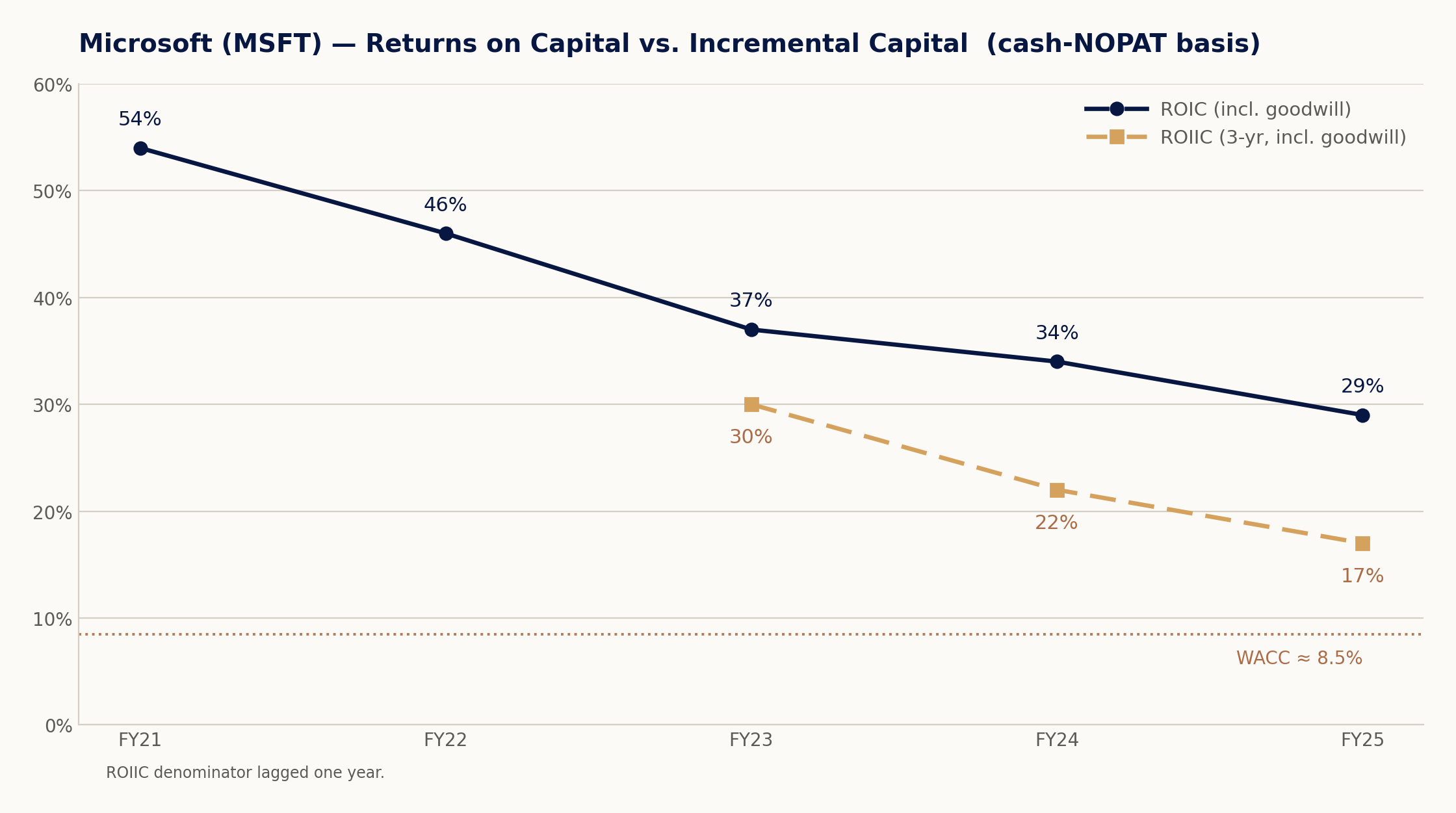

ROIC / ROIIC Breakdown

I build ROIC and ROIIC the Mauboussin & Callahan way: NOPAT off cash taxes, invested capital run both with and without goodwill, and incremental returns measured with the denominator lagged a year (capital you spend today takes ~12 months to show up in profit).

On a cash-NOPAT basis, Microsoft’s return on invested capital is roughly 29% including goodwill and 45% excluding it over the trailing year.

The gap between those two numbers is the Activision deal. $69 billion of goodwill that dilutes the reported figure but not the underlying operations.

I estimate MSFT’s WACC at ~8.5%.

Return on incremental invested capital, the return on the next dollar, has compressed from ~30% to ~17% on a three-year basis, and the most recent one-year reading is roughly 11%.

The AI build-out is burning through capital faster than any returns that capital is producing.

But if this is like a traditional J-Curve investment cycle, ROIIC will reverse as Azure AI revenue catches up to the spend.

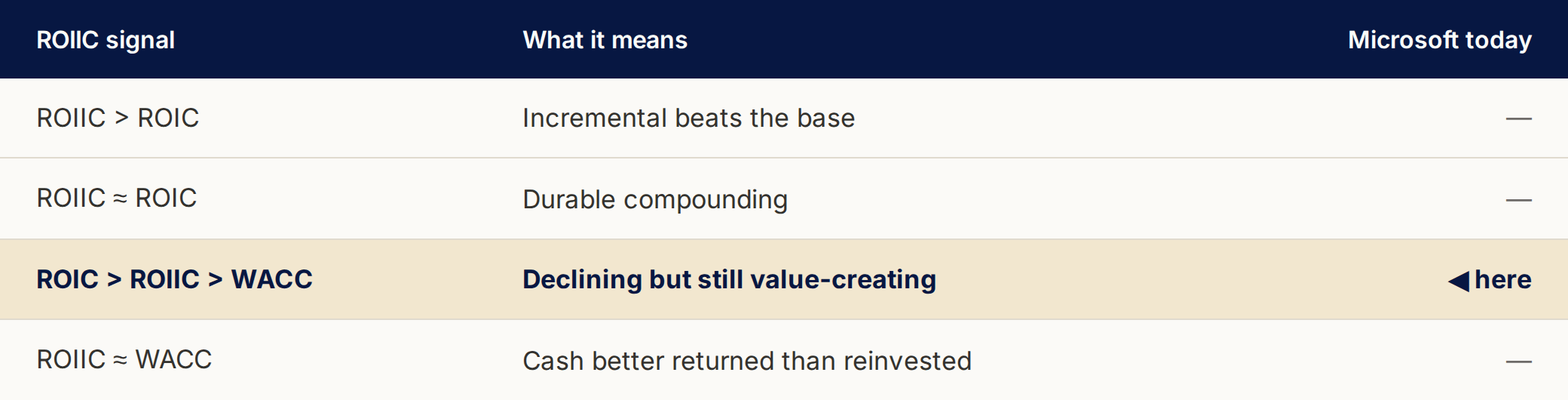

But right now, incremental returns are sliding toward the cost of capital and it’s a key ratio to track.

For a dividend investor this matters a lot.

When the return on reinvestment slips toward the cost of capital, the math starts to favor handing cash back to owners over plowing it back into the business.

Microsoft is doing the opposite, reinvesting harder than ever.

That’s defensible if AI returns show up. If they don’t, the case for a larger dividend and bigger buybacks gets stronger.

Growth Catalysts

Near-term

Sentiment.

The market has knocked Microsoft down roughly a third from its high on one fear: that the AI capex bill arrives before the AI revenue.

Almost anything that narrows that gap flips the narrative, an Azure re-acceleration print, increasing Copilot seat numbers, or the first sign of capex growth plateauing with AI revenue accelerating.

Business.

Capacity is the swing factor. Azure is capacity-constrained, demand exceeds what Microsoft can physically build, so every data center that comes online converts almost directly into billable revenue, and the $627 billion RPO is a backlog waiting to be recognized.

Long-term Secular Growth

Cloud Migration

Public cloud is about 45% of enterprise IT spend today, up from 17% in 2021, and Azure grows ~40% in constant currency into that shift.

AI Monetization

The $250 billion OpenAI Azure commitment, Copilot layering onto the Office base, and triple-digit RPO growth.

But the number a dividend investor should care about most is the reinvestment runway.

The question isn’t whether Microsoft can grow, it’s whether it can keep pouring $65 billion-plus a year into the ground at a high enough return to compound the earnings that fund the dividend.

Right now ROIIC has compressed to ~11% on a one-year basis. The AI runway will be long, but the return on it is, for the moment, mediocre.

If the AI build-out follows a J-curve and incremental returns revert toward the 20–30% the base business earns, Microsoft has a 10-to-15-year runway to compound earnings, and the dividend, at low double digits.

If they don’t, the reinvestment case weakens and the smarter move becomes handing more cash back to owners. Great for the dividend, but the narrative shift would be bad for the stock price.

The core of the bear case is that Azure decelerates, Copilot adoption disappoints, and the capex bill lands well before the revenue. And this is exact gap between spend-now and earn-later that the ROIIC chart is showing today.

Management & Capital Allocation

Satya Nadella has run Microsoft since 2014 and rebuilt it from a stagnant Windows company into a cloud-and-AI leader.

CFO Amy Hood has been beside him since 2013 and their capital allocation has been exemplary. Microsoft returned $42.5 billion to shareholders in fiscal 2025 through dividends and buybacks while still self-funding the largest capex program in its history.

23 years of dividends with consistent raises through three CEOs. Buybacks have shrunk the share count steadily and were generally made at sensible prices.

The M&A record is good: LinkedIn and GitHub are working, the $69 billion Activision integration has been seamless. The old flops (Nokia, aQuantive) are a decade behind and were written down honestly. Insider ownership is modest but that is typical for a company this size.

Peer Comparison

Against its closest large-cap software and platform peers, Microsoft’s profile is the most complete. It’s not the highest yield, not the highest ROIC, but the best blend of return, balance sheet, and dividend reliability.

Salesforce and Alphabet only started paying dividends in 2024, so there’s no comparable track record of consistently paying a dividend.

Oracle has a longer record but carries real leverage and lower returns on capital.

Microsoft is the only name here pairing a 23-year raise streak with a net-cash, AAA balance sheet. It deserves a quality premium to Oracle and Salesforce, and trades at a justified discount to Alphabet’s faster top line.

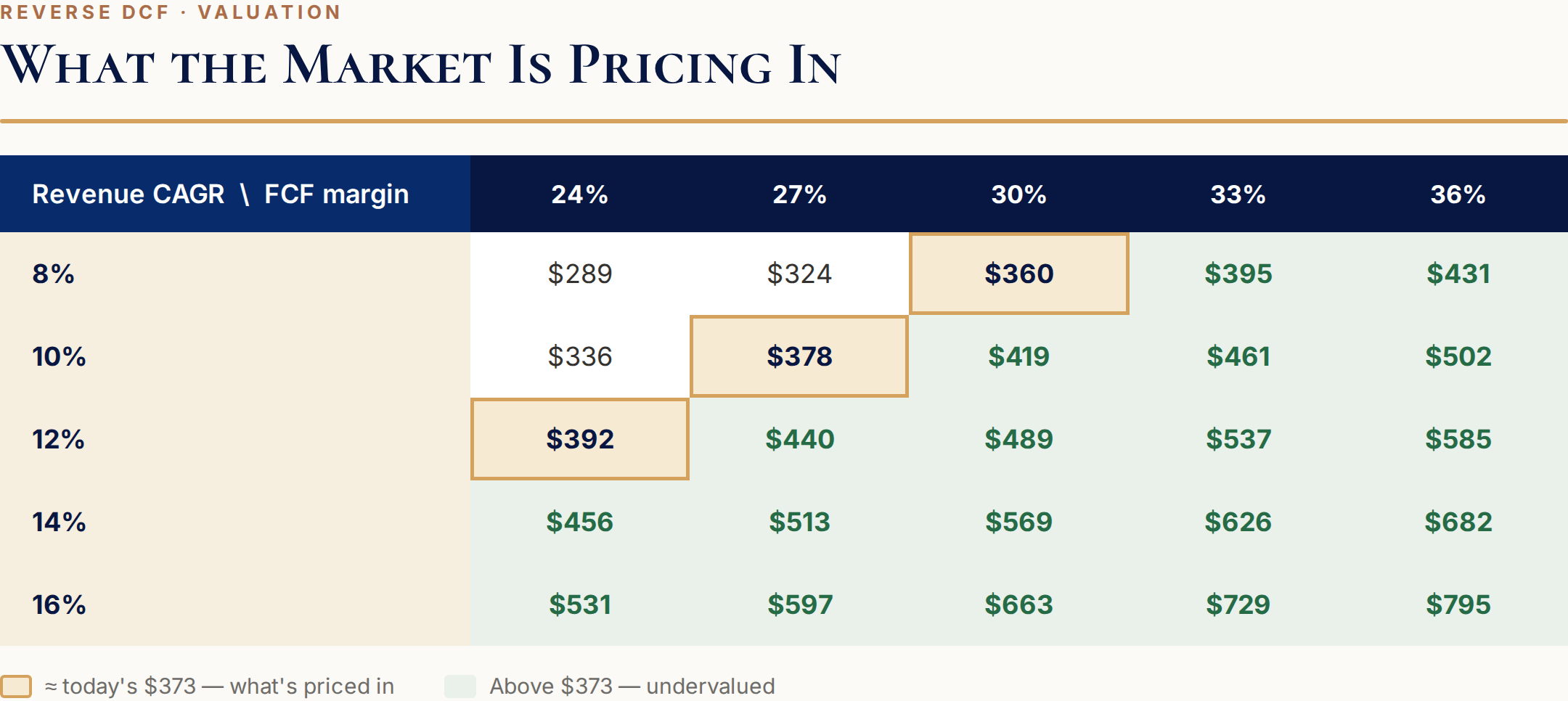

Valuation

Microsoft has fallen from a 52-week high of $555 to $373 (as I write this), roughly down a third.

At $373 you are paying about 22x forward earnings (FY2026E EPS ~$17.20) and ~19x next year’s. Microsoft’s five-year average forward multiple is closer to 32x; the ten-year average near 30x. On EV/EBITDA the stock sits around 13–14x against a historical 24x.

At 0.98%, the forward yield is now above its ten-year average of ~0.97% and well above the five-year average of 0.81%.

Using a reverse DCF, at today’s price the market is implying high-single-digit long-run growth for a wide-moat business that has compounded earnings at low-double-digits and signed $627 billion of future revenue.

MSFT doesn’t deserve a peak multiple given the ROIIC compression and spending 25% of revenue on capex until those returns turn. But even my conservative base case leaves Microsoft meaningfully undervalued today.

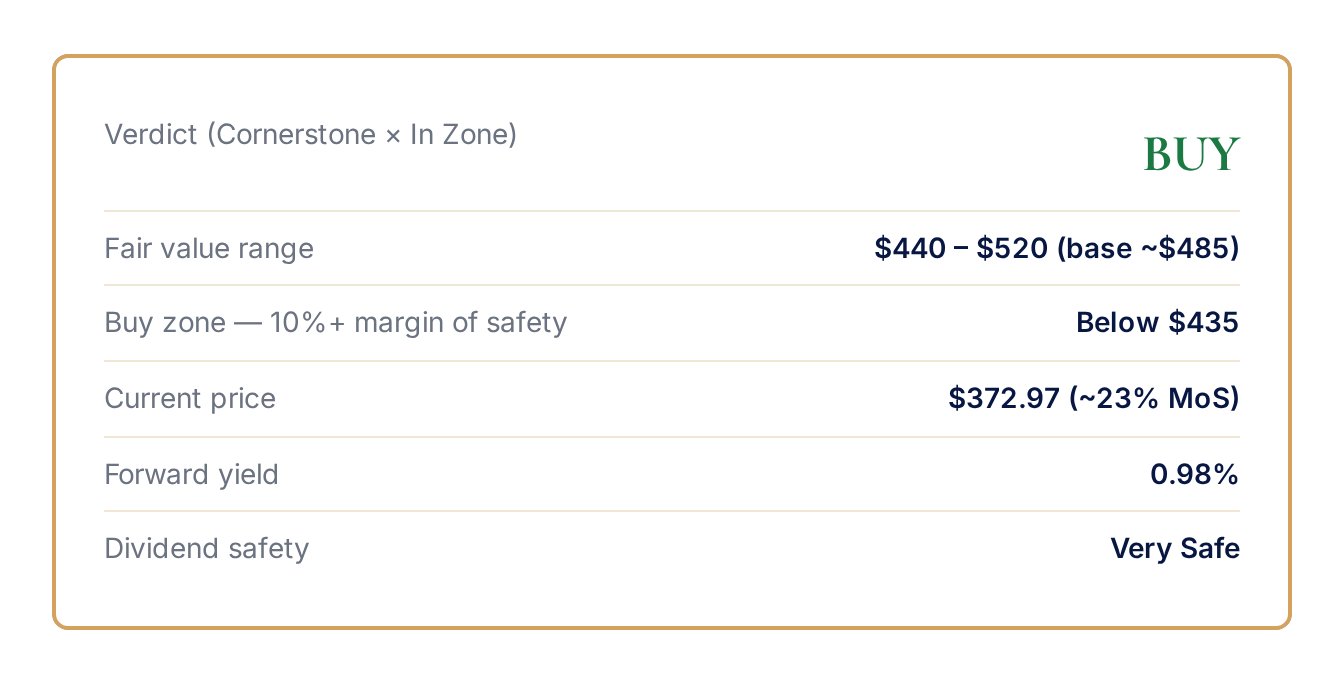

The Verdict & Buy Zone

Microsoft misses Gold Standard by a single point because of two valid reasons.

It isn’t a Dividend Aristocrat for two more years, and the AI build-out is bending its incremental returns toward the cost of capital.

Until these change, MSFT is a Cornerstone. The kind of name you anchor a portfolio with and add to on exactly the weakness the market is handing you right now.